The Inland Revenue Authority of Singapore (IRAS) adopts a proactive approach in providing timely education and assistance to taxpayers so that they can take an active role to fulfil their tax obligations.

This is currently the season to file your individual income tax returns and here are some filing tips and information that we would like to share with you. With this information, you will be able to file your tax returns confidently and accurately.

Filing tax returns: salaried employees/self-employed taxpayers

Salaried employees

If you had received a "No-Filing Service" letter or SMS, you probably did not have to e-file your tax returns by 18 April 2018 unless you had other sources of income (eg, director's fees, honorariums) on top of your automatically included employment income; if your relief claims (eg, child relief) have changed; or if you wish to claim for course fees. Assuming that you did not need to file your tax returns, a Notice of Assessment would be automatically issued to you based on the income information sent to IRAS by your employer and your relief claims for last year. However, the reliefs may subsequently be adjusted by IRAS if you do not meet the eligibility criteria.

Your employment income will automatically be included in your tax returns if your employer is participating in the Auto-Inclusion Scheme (AIS). You can check the list of employers who are on the AIS here: https://goo.gl/Qp5cph. You do not need to include these automatically included employment incomes in your tax return.

Self-employed income

If you are a self-employed medical practitioner, you should declare your income under "trade, business, profession or vocation" instead of "other income". If you are a medical practitioner who is engaged as salaried employee, but also receive income as a locum or from other consultations, you should also declare such income under "trade, business, profession or vocation".

Generally, a self-employed person needs to prepare a two- or four-line statement for income tax reporting purposes, depending on the revenue of the business. A four-line statement would consist of the following and is required when the revenue exceeds $100,000 but less than $500,000:

- Revenue (total payments/fees received or receivable for services provided and goods sold before deducting any expenses)

- Gross profit/loss (revenue less cost of goods sold)

- Allowable business expenses (please refer to IRAS website for the qualifying conditions)

- Adjusted profit/loss (gross profit/loss less allowable business expenses)

In addition to the above, a certified statement of accounts, to be signed by the sole-proprietor or precedent partner stating that it is true and correct, needs to be submitted if the revenue exceeds $500,000.

If the revenue is below or equal to $100,000, only a two-line statement showing the revenue and adjusted profit/loss is required.

Keeping proper records

For information relating to the keeping of proper records, please visit https://goo.gl/HpxTa2.

Do you need to register for GST?

Compulsory GST registration

You are required to continually assess whether your business needs to be registered for Goods and Services Tax (GST) compulsorily. In most cases, registering for GST is compulsory when your taxable turnover for the past four quarters is more than $1 million (unless you are certain that business turnover in the next 12 months will not exceed $1 million) or if you can reasonably expect your taxable turnover in the next 12 months to be more than $1 million.

If your situation is either of the above, you need to apply for GST registration within 30 days of the date when your registration liability arises.

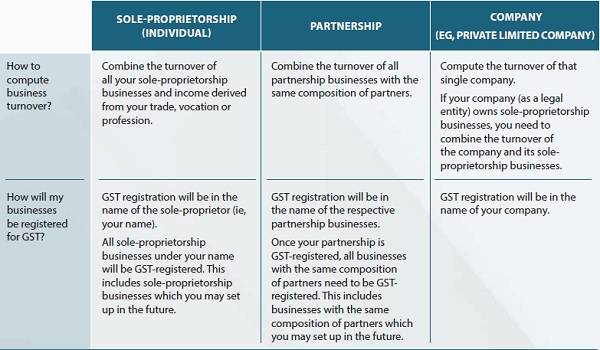

Computing your business turnover

The method used for computing business turnover for GST registration purposes depends on your business setup (eg, sole-proprietorship, partnership, private limited company). Refer to the table below for more information.

Can you charge GST when you are not GST registered?

Only GST-registered businesses are allowed to charge and collect GST on their supply of goods and services. If you are a non-GST registered business, you are not allowed to charge GST.

If you are not registered for GST and have wrongfully collected GST from your customers, you should stop this practice immediately. You are required to quantify and remit the amount of GST wrongly charged on your invoices to the Comptroller of GST.

Are you displaying prices correctly?

GST-registered businesses must show GST-inclusive prices on all price displays (eg, price tags, price lists, advertisements, publicity brochures and websites). Prices that are quoted, whether written or verbal, must also be GST-inclusive. Price displays with a qualifying clause that prices are before GST or are subject to GST are not acceptable.

Voluntarily disclosing past mistakes

IRAS believes that taxpayers are generally compliant and that most cases of non-compliance arise from negligence or insufficient understanding of tax matters. We encourage taxpayers who have made errors or submitted incorrect returns to come forward voluntarily in a timely manner, to disclose these errors or omissions and get their tax obligations right. By doing so, they may qualify for our Voluntary Disclosure Programme, under which the penalty for such errors or omissions will be greatly reduced. For more details, please refer to https://goo.gl/7dAoHi.

Common tax mistakes made by medical practitioners

Through the audits we have conducted on medical practitioners over the past few years, we noticed some common mistakes that medical practitioners tend to make (as seen below).

Understatement of income

Gross consultation fees and revenue received from prescriptions and sales of medicine were not reported in full. You are required to maintain proper records of all fees/revenue received so that the revenue amount can be correctly reported. Fees charged to patients for laboratory/x-ray tests should also be reported as revenue regardless of whether a profit is made.

Income received as a locum should also be reported as trade income. The payer should issue statements to the locums to aid them in reporting the income in their tax returns.

Employment income, such as salaries, bonuses or director's fees received by medical practitioners who are employees or directors in companies, should also be reported under the "Employment Income" section in the income tax returns.

Incorrect claim of expenses

Private and domestic expense claims such as personal insurance, expenses incurred for personal trips, family holiday expenses, personal medical expenses, private entertainment expenses, and domestic utility and telephone charges are not deductible for income tax purposes.

Unsubstantiated claims of payments to suppliers or of disproportionate amounts of salary made to family members are disallowed. Payments made to family members who are helping out with the business should be pegged to market rates and the salary paid must commensurate with the work and duties of the family member. Taxpayers must also keep complete and proper receipts and tax invoices to show that the expenses are incurred for business purposes.

Claiming of expenses based on estimations and without any valid basis is incorrect. Claims of expenses against income should be made based on actual amounts incurred for the business, with supporting receipts and invoices. Sketchy records, with merely approximate amounts, are inadequate and not acceptable for income tax/GST purposes.

Claims of private motor vehicle expenses for private cars (E- or S-plate), including petrol, insurance, repair and maintenance, parking and Electronic Road Pricing charges, are not allowed under the Income Tax Act. These private car expenses are not allowed even if they are incurred for business purposes.

Tax avoidance arrangements

A tax avoidance arrangement normally involves an arrangement that is artificial, contrived or has little or no commercial substance. Such an arrangement is typically designed to obtain a tax advantage that is not intended by Parliament.

Some examples of tax avoidance arrangements observed by the comptroller include:

(i) Setting-up of more than one entity for the sole purpose of obtaining tax advantage;

(ii) Change in business form for the sole purpose of obtaining tax advantage; and

(iii) Attribution of income that is not aligned with economic reality.

The comptroller will disregard and make relevant adjustments to arrangements which are carried out with tax avoidance as one of their main purposes and are not for bona fide commercial reasons. For information relating to tax avoidance arrangements, please refer to The General Anti-avoidance Provision and its Application (First Edition) at https://goo.gl/3EZCwU.

Failure to maintain business records for a period of five years

Some taxpayers have failed to keep and retain sufficient records to enable IRAS to ascertain their income and allowable business expenses. The common misconception is that they do not need to keep records or can discard their records once a Notice of Assessment is received. This is incorrect. The records should be retained for the requisite period of five years whether or not an assessment has been raised. The comptroller may request for these documents in the course of audits.