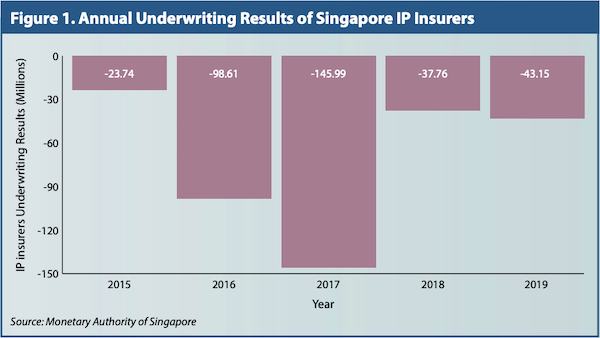

There has been persistent unhappiness among doctors about insurers and third-party administrators (TPAs). Accusations abound of erosion of professional autonomy and cut-throat rates offered. On the other hand, rising premiums are causing a furore among the public with the insurers justifying them by pointing to continued losses (Figure 1) and increasingly higher claims.

The truth often lies somewhere in the middle and we can understand both vantage points better by going back to first principles.

Where is the money in insurance?

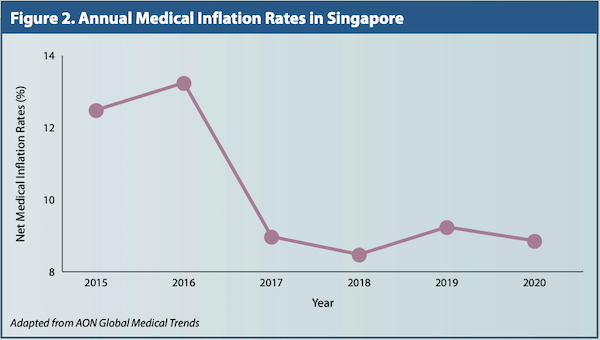

Insurance at its heart is about risk pooling. Healthcare can be very expensive and virtually nobody can afford to pay for healthcare out of savings. Hence insurance provides a valuable societal function by collecting monies in the form of premiums and channelling them to those faced with high medical expenses. What about TPAs? Well, healthcare costs have been rising faster than general inflation (Figure 2) and TPAs market themselves as a means for administrative ease for payers, such as insurers and employers, thus cutting down costs.

How do TPAs do this? Firstly, through economies of scale and specialisation, by carrying out claims processing more efficiently than payers could do themselves. Many insurers focus on selling more policies and brand management, preferring to leave the work of driving cost efficiency in claims processing and engaging doctors to TPAs. Secondly, TPAs negotiate for better rates and finally, TPAs also scrutinise bills and on occasion decline to make payouts if the claim is deemed beyond "reasonable and customary".

A payer's market

Payers think in relatively simple terms when it comes to healthcare claims; it's just the total number of claims multiplied by the average amount per claim. Hence, to control healthcare costs, reduce one or both drivers and TPAs position themselves well for both.

Unfortunately for us doctors, one man's meat is another man's poison, as they say. Reducing claims and amount per claim effectively reduces payments to healthcare providers! We thus naturally resist.

Some of the common ways to bring down costs would be empanelment, by narrowing the choice of doctors to a smaller number that have agreed to lower consultation fees and are more price-friendly to payers. The quid pro quo then has to be higher volumes for favourable pricing and easier administration. Hence insurers and TPAs would determine optimal panel sizes to cover what patients need and not grow beyond that – payers win through better pricing, doctors get more patients, and patients/policy holders have easier claims administration.

However, for doctors who are not on the panels, it is very tough as their patients then face challenges obtaining care from them and are instead encouraged financially or otherwise to seek care from empanelled doctors. The reality now is that it is a payers' market and we can expect insurers and TPAs to get more and more forceful in managing costs. We doctors on the other side are so poorly organised as a group that there is little collective voice. I'm not sure how much solidarity there would be for all doctors to "boycott" any particularly pugnacious TPA or insurer either.

Striking a balance

What about insurers or TPAs that deny claims and challenge the medical necessities which doctors carry out on an almost daily basis? In our opinion, we don't think insurers have the expertise nor should they be doing this, but we as a profession need to manage ourselves and censure the black sheep among us. How about a professional body with the required expertise and credibility taking up the challenge of establishing appropriate practice guidelines for, say, endoscopy use and other high volume procedures? And also to work with the insurers and TPAs to review the actual data of every doctor with an eye to appropriateness and fair pricing? I suspect insurers and TPAs do not want to get into the "down and dirty" details of clinical practice, but when faced with escalating claims and no viable alternatives, what choice is there?

Experienced doctors would be able to relate that as with any relationship, trust is built up over time. Practising within the norms, including in pricing, greatly eases interactions with insurers and TPAs. One senior surgeon told me that he charges at the 50th centile and always calls the insurer for any cases out of the ordinary; he reported no issues with any of the insurers.

We as a medical profession need the insurers to risk pool and help our patients to afford healthcare. The insurers need us as no insurer, no matter how big or powerful, can actually treat patients. Do we need TPAs? That's a naughty question which we can't answer directly, but look at the reasons for being. If these cease to be relevant...

How do we reset this acrimonious relationship between us and the insurers? Let's agree that we need each other to not only survive but thrive, and that we need to ensure both parties are fairly treated. Respect and autonomy for doctors, fair pricing and predictable on-average claims experience for insurers, and an efficient and reasonably amicable administrative process for everyone.