SMA conducted the second iteration of a survey to rank the Integrated Shield Plan (IP) providers (namely, AIA, AXA, Great Eastern, NTUC Income, Prudential, Raffles Health Insurance, and Singlife [formerly Aviva]). Respondents were asked to provide their views for the time period of January 2022 to December 2022.

The survey opened on 17 February 2023 and, at the closing of the survey on 16 March 2023, a total of 152 complete responses were received. A response is considered complete when all questions are answered, including selecting N/A (ie, Not Applicable) as a response. Respondents were required to submit their unique Medical Registration Number (MCR number) for verification purposes and to prevent a doctor from responding to the survey more than once.

The survey sought to obtain respondents' opinions on their experience with the various IP providers, in terms of inclusiveness of panels, transparency of doctor selection criteria for panels, and more (visit https://bit.ly/IPsurvey2022 for the full survey form).

A new question was added to the list of questions used in the latest edition of the survey:

In terms of likelihood of you recommending your family members, friends and relatives to buy a IP policy from these IP providers, please rate the following IP providers, 1 being the least likely and 5 being the most likely.

All other questions were left unchanged to allow for comparison across the two surveys. The report of the first survey can be found at https://bit.ly/5404-Survey.

For most of the questions, a weighted average system was used, with the total scores divided by the number of responses. Respondents were asked to respond using a scale of 1 to 5, with 1 being the lowest, 3 being the midpoint, and 5 being the highest. An N/A option was also available to respondents. The answers from respondents who selected the N/A option were not factored into calculating the weighted average. An example of how the weighted average was tabulated is as follows:

53 respondents rated IP X "1" (53 x 1)

21 respondents rated IP X "2" (21 x 2)

30 respondents rated IP X "3" (30 x 3)

42 respondents rated IP X "4" (42 x 4)

43 respondents rated IP X "5" (43 x 5)

5 respondents selected N/A

Total score = 568

Total respondents (excluding those who chose N/A for the question) = 189

Weighted average = 568 / 189 = 3.005, rounded off to 3.01

Results

The survey asked respondents for their names, MCR numbers and email addresses for verification purposes. Following which, respondents were asked to indicate if they were a GP/ Family Physician/Locum, a Specialist, or Others (eg, medical administrators working in hospitals, healthcare companies, insurance companies, third-party administrators, Ministry of Health [MOH], statutory boards, medical schools), as well as whether they worked in the private or public sector.

As IP contracts are usually signed on by specialists in the private sector, we had expected the majority of respondents to be represented by them – of the 152 respondents, 82% were specialists and 97% were from the private sector. This is similar to the 2021 survey where 87% of respondents were specialists and 98% were from the private sector.

Respondents were then surveyed on an array of questions with respect to their experience with the seven IP providers. The summary and discussion of the results are as follows:

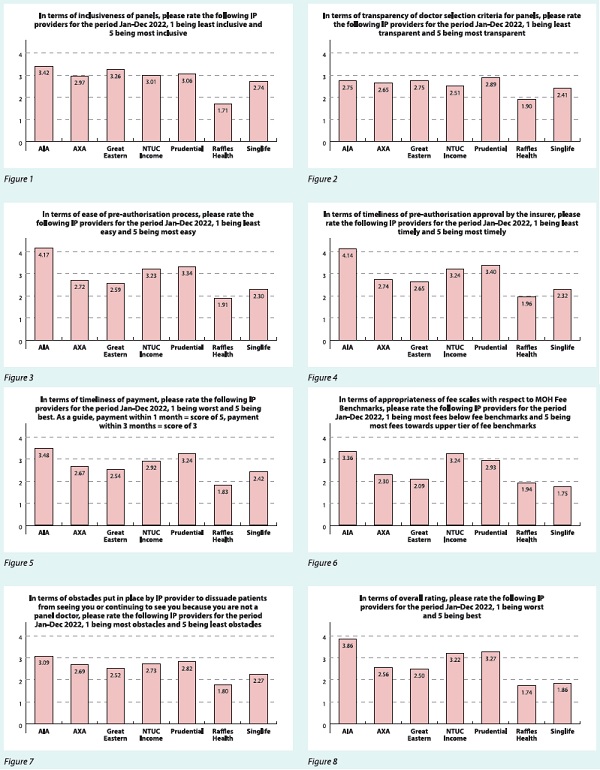

- IP providers were rated in terms of inclusiveness of panels, with the majority scoring above the midpoint of 3 (see Figure 1). This is an improvement over the previous surveyed period of January to December 2021, which had only one provider scoring above the midpoint.

- In terms of the transparency of doctor selection criteria for panels, none of the providers passed the midpoint (see Figure 2). This is similar to the responses received for the previous surveyed period.

- Three out of the seven IP providers scored above the midpoint in terms of ease of their pre-authorisation process (see Figure 3). This is similar to the results for the previous surveyed period.

- Similarly, three providers scored above the midpoint in terms of timeliness of pre-authorisation approval (see Figure 4). This was the same for the responses received for the previous surveyed period.

- Respondents were asked to rate the IP providers in terms of timeliness of payment, with the score of 5 indicating payment within one month and 3 being within three months. Two out of the seven providers were able to pay within an average of three months, with no provider paying within one month (see Figure 5). This is similar to the results for the previous surveyed period.

- When IP providers were rated in terms of appropriateness of fee scales with respect to the MOH Fee Benchmarks, with a score of 1 being most fees below fee benchmarks and 5 being most fees towards upper tier of fee benchmarks, two providers passed the midpoint (see Figure 6). This is a slight improvement over the previous surveyed period, where respondents indicated that only one provider passed the midpoint.

- In terms of obstacles put in place by the IP provider to dissuade patients from seeing the respondent if he/she was not a panel doctor, only one provider was able to reach the midpoint (see Figure 7). This is a slight improvement for responses over the previous surveyed period, where none of the providers were able to reach the midpoint.

- Three out of the seven providers scored above the midpoint in regard to their overall rating (see Figure 8). This is similar to the results for the previous surveyed period with the same number of providers scoring above the midpoint. For comparison, the change in weighted average scores for the IP providers over the two surveys are highlighted below.

-

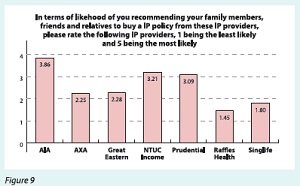

Finally, on the question of the likelihood of respondents recommending their family members, friends and relatives to buy a IP policy from the listed providers, three of the seven providers scored above the midpoint (see Figure 9).

Conclusions

In the first survey, we obtained a total of 210 complete responses. In this latest survey, we obtained 152 complete responses.

As had been previously announced, IP providers who had less than 30 responses to any question were excluded in the results. However, no IP provider fulfilled this exclusion criterion for any question.

Notwithstanding the above, based on responses received, we see slight improvements in three areas:

While we see several initiatives arising from the Multilateral Healthcare Insurance Committee, of which SMA is a member, there is a risk of momentum slowing down as policymakers start to focus on other initiatives while regulation continues to be inadequate.

SMA's stance remains the same: As long as doctors follow the fee benchmarks, there should not be a need for panels. The current setup still results in unnecessary friction, if not obstacles, to the delivery of good medical care for patients.

In the meantime, insurance premiums continue to rise, and patient access to care remains a concern. SMA will continue to scrutinise the health insurance industry, to help both patients and doctors alike.