SMA 61st Council Position Statement on Troubled Integrated Shield Plans (IPs)

1 The SMA Council is of the opinion that the Integrated Shield Plan (IP) insurers, must take much of the responsibility for the quagmire they find themselves in: where IPs with as-charged and first-dollar comprehensive riders have consequentially higher and more frequent claims by policyholders. This is because these riders were introduced by IP insurers, and with knowledge of the consequences of such riders which have been well known in the industry for a long time. The SMA Council agrees that to address this, co-payments and deductibles have to be re-introduced, but this does not detract us from the fact that this problem was created by the IP insurers, in the first place.

2 While the SMA Council still supports in-principle, the recommendations found in the Health Insurance Task Force (HITF) Report, it wishes to make clear that it is unable to support how the Life Insurance Association (LIA) and many of its members have chosen to implement these recommendations. These include:

a) Highly exclusive panels where many IP insurers only have about 21%1 of private specialists on each panel

b) Opacity in the selection criteria for doctors to be included as preferred providers in panels

c) Other than one insurer, other IP insurers do not respect both the higher and lower limits of fee benchmarks; their fee scales are clustered around the lower limit only.

3 The SMA Council is of the opinion that the current IP sector appears to be loss-making or unsustainable NOT because of excessive or higher claims by policyholders. This is evidenced by the fact that for the period 2016 to 2019:

a) The estimated Average Payout Per Claim went down by 1% from 2016 to 20192 . There could be many reasons for this, but obviously the size of payout has been stable for these recent four years;

1 Joint AMS-CFPS-SMA letter to MOH, The Aftermath of the HITF Report, Annex: Comparison of Panel Doctors vs Number of Specialists, Sep 2020

2 Medishield Life 2020 Review: SAS Comments, Table 2.1.3 https://actuaries.org.sg/sites/default/files/2021-01/SASResponseMSHLReview2020FINAL.pdf

b) The claims incidence rate for IPs has been growing at a Compound Annual Growth Rate (CAGR) of 9%2 , which is comparable to the Medishield Life’s corresponding rate of 10%.

4 For the period 2016 to 2019, the growth in Management Expenses (56.6%) and Commission (50.4%) consumed by IP insurers have far outstripped that of Gross Claims (35.9%) 3 . This rapid rise in Management Expenses and Commission seems to be the key factor for the sector remaining unprofitable and unsustainable in the last few years.

5 All stakeholders should note that one of the key features of the current IP environment is that it is indirectly subsidised by the government when IP policyholders voluntarily downgrade to subsidised wards in restructured hospitals when they are entitled to higher ward classes, that is, “voluntary down-graders”.

6 The SMA Council recommends that the relevant authorities look into the possibility of improvement of the current claims ratio of 75%, to ensure that premiums collected are not excessively spent on non-healthcare cost items and, also to instil cost discipline in IP insurers.

7 To improve the long-term sustainability of the IP sector, the SMA Council is of the opinion that measures to reduce administrative and manpower costs in the IP sector be explored. For example, reduction of the number of payors will be more efficient and reduce duplication in resources and costs when compared to the current situation. Savings so generated can be used to mitigate future increases in insurance premiums.

8 In the meantime, the SMA Council will introduce two initiatives

a) Ranking of IP insurers, and

b) Setting up of a Complaints Committee for IPs and Health Insurance.

9 The SMA Council is grateful that the Minister of Health has agreed4 with Dr Tan Yia Swam, that we can all benefit from more information-sharing and a better understanding of insurance products. The SMA urges the Ministry of Health (MOH) and the Monetary Authority of Singapore (MAS) to publish more data on individual IP insurers to educate stakeholders and the public who are considering buying an IP.

10 The SMA Council will continue to work with MOH as well as its sister organisations, the Academy of Medicine, Singapore and the College of Family Physicians Singapore, to ensure that the interests of the public, IP policyholder and IP patient are protected and best served.

3 paragraph 24, main document of SMA 61st Council position statement on Integrated Shield Plans

4 Minister for Health, Committee of Supply, 3.30pm onwards https://sprs.parl.gov.sg/search/sprs3topic? reportid=budget-1630

SMA 61st Council Position Statement on Troubled Integrated Shield Plans (IPs)

1 In the past few months there has been a lot of discussion on how viability of the existing IP arrangements, on which about 70% of Singapore residents rely, may be more assured. In theory here are three broad areas of possible improvement: (a) Collecting higher premiums, (b) controlling costs, and (c) reducing coverage. The emphasis so far taken by the Life Insurance Association (LIA) has been on one aspect of controlling costs, namely that of retaining just a small panel of doctors selected for low cost and easy monitoring, and reimbursing doctors at low rates through these panels. The down-side of this approach, when an insured person becomes a patient and is pressured to changing from his personal doctor, is obvious. This paper tries to explore whether there are other directions of controlling costs beyond curtailing doctor choice, so that the highly unpopular alternatives (higher premiums and lower coverage) may be less impacted.

Historical Context

2 The following is a chronology of important milestones in the history of IP development in Singapore:

a) IPs have been in place since 1994 when NTUC Income introduced IncomeShield.

b) Co-payment and deductibles were features that were present in the IP policies that were sold between 1994 and 2005.

c) As-charged plans were first offered in 2005, and first-dollar coverage riders were offered in 2006, even though the consequences of such coverage protection were well known5 in the insurance industry.

d) The SMA Guidelines on Fees (GOF) was withdrawn in 2007 and doctors and patients were left without general guidance as to what fees were reasonable and customary.

e) The Health Insurance Task Force (HITF) was set up in 2015 (to try to control resultant escalating costs) and the report was published in 2016.

f) The Ministry of Health (MOH) fee benchmarks were published in 2018, re-establishing guidance for “reasonable fees” as a follow-up to the HITF report.

A The Issue of Rising Claims with Comprehensive and As-Charged Riders

3 There is a common narrative to vilify the patient and the doctor and hold them accountable for the current situation whereby IPs with comprehensive as-charged and first-dollar riders experience higher claim sizes (“payouts”) and claim incidence (“frequency”).

4 While it is true that such IPs do experience higher payouts and claim frequency as compared to those that do not have such riders, this only tells half the story.

5 There is abundant literature6 to show that overconsumption of healthcare services is likely to occur when deductibles and co-payment are removed when claims were made. The first ascharged plans were made available in 2005 while first-dollar coverage riders were introduced in 2006. All IP insurers soon offered such features in their IP product offerings. They did so voluntarily for reasons best known to them; but the fact is they were not compelled to do so by any third party.

6 In 2007, the Singapore Medical Association (SMA) was told that its Guidelines on Fees (GOF) contravened the Competition Act, which led to the GOF being reluctantly withdrawn7 by SMA. The SMA warned all stakeholders of the possible negative consequences of withdrawing GOF, which included doctors charging more than what they would have, had GOF remained. Unfortunately, these warnings were not heeded.

7 Even so, despite murmurings in some quarters that overcharging is not uncommon in Singapore, it is also important to note that since 2007, there has only been one case of a doctor being punished by the Singapore Medical Council (SMC) for overcharging; the SMC’s decision in this case was affirmed by the Courts8 .

8 In highlighting that doctors and patients are responsible for the situation whereby IPs with as-charged riders and first-dollar comprehensive coverage come with higher payouts and claim frequency, the LIA and insurers conveniently ignore the fact that all these would not have come about had the insurers not offered such riders in the first place. Doctors and patients are also economically rational human beings and will respond to such riders. Once these riders are in place, an economically rational healthcare provider will likely charge more and an economically rational consumer will consume more so as to maximise their benefit and utility from the system. To quote Deming, “Every system is perfectly designed to get the results it gets”.

6 Example 1: RAND Health Insurance Experiment https://www.rand.org/health-care/projects/hie.html, Example 2: “...Integrated Shield Plan (IP) full riders which cover the entire co-payment under the IP plan, have contributed to higher medical/hospitalization bill sizes.” https://www.moh.gov.sg/news-highlights/details/correlation-betweenquantum-of-medical-bills-and-medical-insurance-coverage

7 SMA News, Apr 2007, President’s Forum https://www.sma.org.sg/UploadedImg/files/Positions%20Statements/Withdrawal_SMA_Guideline_on_Fees_Presiden tsForumApr07.pdf

8 Lim Mey Lee Susan v Singapore Medical Council [2013] SGHC 122

9 Therefore, it is important to state that doctors and patients are just behaving as economically rational beings would in an as -charged and first -dollar coverage environment that was entirely created by IP insurers alone. IP insurers have to accept most of the responsibility for this quagmire they have found themselves in.

B Health Insurance Task Force (HITF) Report and Recommendations

10 The SMA was represented in the HITF and the Report9 was published in October 2016. The LIA's letter10 to The Straits Times Forum on 18 March 2021 stated "The Health Insurance Task Force (HITF), which included the Singapore Medical Association (SMA), recommended a suite of measures to do so, including panels, pre -authorisation, fee benchmarks, and co -pays".

11 There were several other parties in the HITF but the LIA chose to single out the SMA in the letter. The SMA Council has stood by the recommendations11 of the HITF and hopes the LIA, and every of LIA's members who are IP insurers, would do likewise. We should not just support the form but the substance of each recommendation as well.

12 For example, the Report stated that panels can be formed. It is therefore reasonable that the inclusion and exclusion criteria for choosing a preferred provider should be clear. To-date, despite multiple engagements with the LIA, not one IP insurer has done so.

13 The HITF Report stated "To enhance and ensure transparency of the arrangement (e.g. disclosures on the healthcare provider selection process)", that is, IP insurers should state the criteria used to select doctors to be on a panel. The fact remains that no doctor or policyholder knows what the actual quantitative or qualitative measures that make up these secret criteria are.

14 A study conducted by the Academy of Medicine, Singapore in June last year revealed that each insurer's IP panel only had about 21% of private specialists12. In other words, a policyholder may only have pre -authorised access to only 21% of private sector specialists. We recognise that this data may be slightly out of date, and we would invite LIA to release the latest such information of the IP insurers so that the public may know exactly what proportion of private sector specialists are on each IP panel.

15 Since there are MOH fee benchmarks in place now to address overcharging, there is no reasonable justification for highly exclusive panels. Panels, if needed, should be inclusive in the first instance and private sector specialists should be excluded only if they have a poor track record.

16 MOH fee benchmarks have been published for the commonest 222 procedures since late 2018. Each benchmark for a procedure comes with a lower and an upper limit. Only one insurer fully respects the entire span of the benchmarks (that is, both the upper and lower limits). The other IP insurers' fee scales are clustered around the lower limit. If the LIA and IP insurers are sincere about respecting the MOH fee benchmarks, then they should not be reimbursing at rates that only approximate the lower limit. In fact, most are not even reimbursing at the mid -point of the benchmarks, that is, halfway between the lower and upper limits. If they are sincere in respecting the HITF Report recommendations, they should not cherry -pick around the lower limit. They should respect the upper limit as well. This is another example of LIA and IP insurers adhering to the form but not the substance of the HITF Report. We also note that one IP insurer persists in reimbursing below the lower limit.

17 It should also be noted that respecting MOH fee benchmarks should be such that the actual fees paid to service providers are within benchmarks, and not include fees that are taken by third party administrators (TPAs) as well. Several IP insurers use TPAs to run their IP programmes. TPAs' fees should not be taken into consideration when one determines whether an IP insurer respects the MOH fee benchmarks or not.

18 While the SMA Council continues to support in -principle the HITF Report's recommendations, the SMA Council wishes to make clear that it is unable to support the way how the LIA and many of its members have implemented these recommendations. These include:

a) Highly exclusive panels where many IP insurers only have about 21% of private specialists on each panel

b) Opacity in the selection criteria for doctors to be included as preferred providers in panels

c) Other than one insurer, other IP insurers do not respect both the higher and lower limit of fee benchmarks; their fee scales are clustered around the lower limit only.

C The Sustainability of IP as a Health Financing Tool

Points Raised in Parliament

19 About 70% of Singapore residents have bought an IP. This is a very high penetration rate. There are some unique features about IPs that were brought up by SMA President and Nominated Member of Parliament, Dr Tan Yia Swam in Parliament in Mar 202113 and it bears repeating here:

"A more difficult but important policy question to ask is what proportion of Singapore Residents should buy IP. The combined market share of private hospitals and A class and B1

13 Dr Tan Yia Swam, Committee of Supply, 2.45pm onwards https://sprs.parl.gov.sg/search/sprs3topic? reportid=budget-1630

class beds in Restructured Hospitals is estimated to be in the range of 30% to 35%. Yet the proportion of Singapore Residents buying an IP is nearing 70%. This is an unusual phenomenon in the running of a health insurance system. In the normal scheme of things, healthy insurance policyholders subsidise policyholders that fall sick and make claims. But in our IP environment, the business of IP is cross -subsidised not just by those who don't fall sick, but by those who do fall sick and yet choose to treated at subsidised 82 and C classes in restructured hospitals when they are entitled to more under their IPs. At the superficial level, it would appear that there is nothing wrong with this because it is the patient's choice and it is good to be prudent. However, there is an externality cost to IP holders choosing subsidised wards in the Restructured Hospitals when the fall sick. The consumption of these government subsidies are indirectly subsidising the insurers' IP businesses and depriving poorer patients of more subsidies, since MOH's budget is a finite thing. This is because these government subsidies would not have been consumed had the IP providers chosen what they were entitled to, to be treated in the private hospitals or in A or 81 class wards. Another important corollary of this unusual phenomenon is it further lengthens the waiting times for subsidised services in restructured hospitals".

20 She further said, "We need to be clear about what is desired proportion of Singapore Residents who should buy IPs. Is it the current 65% to 70%? Or below or above this range? I do not know the correct figure, but my gut feel is that with a private sector market share of only 30 to 35%, including B1 and A class beds in restructured hospitals, the corresponding figure of 70% of the population having IPs sounds rather high. Can the private sector support the needs of these 70% if all of them who fell ill chose the unsubsidised services they are entitled to under their IPs?

21 It remains to be seen what is a sustainable market penetration rate for IPs. Can the current IP environment be considered to be sustainable when it is indirectly subsidised by taxpayers' money in the form of subsidies consumed by voluntary "down -graders" in restructured hospitals?

22 Dr Tan Yia Swam also made a call for more transparency and that MOH can collate data from various IP providers on how many percentage of private specialists are on each IP panel and how each IP pays specialists when compared against the MOH fee benchmarks. The SMA Council is grateful that the Minister for Health has responded positively to this suggestion.

The Singapore Actuarial Society's Comments

23 A presentation published on 29 Jan 2021 by the Singapore Actuarial Society (SAS) titled "Medishield Life 2020 Review: SAS Comments"14 made many interesting observations using data obtained from MAS. These include:

a) The Average Payout Per Claim went down by 1% from 2016 to 201915. There could be many reasons for this, but obviously the size of payout has been stable for these recent four years.

b) The claims incidence rate for IPs has been growing at a Compound Annual Growth Rate (CAGR) of 9%, which is comparable to the Medishield Life's corresponding rate of 10%.

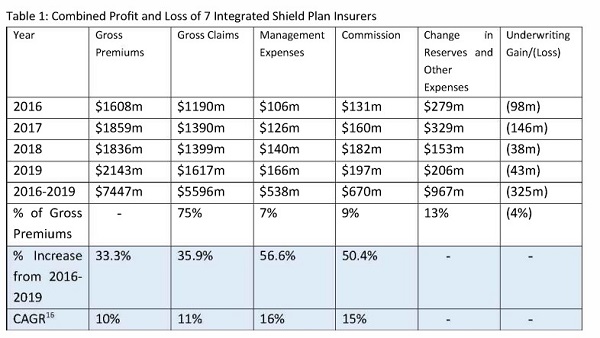

24 We further reproduce a table that was in this abovementioned presentation:

Table 1: Combined Profit and Loss of 7 Integrated Shield Plan Insurers

25 The last two rows are additional observations made by the SMA Council. It clearly shows that Management Expenses and Commission have grown at a much faster rate than Gross Claims and Gross Premiums.

26 Management Expenses and Commission are what the insurer pays itself and its insurance agents to run its IP programmes and services. The growth rates in these two categories have far outstripped the growth rate of monies paid out to healthcare providers. We suggest that the IP industry should take a hard look at how it justifies its management and commission costs as the first step in ensuring the IP industry is sustainable.

14 https://actuaries.org.sg/sites/default/files/2021-01/SASResponseMSHLReview2020FINAL.pdf

15 Medishield Life 2020 Review: SAS Comments, Table 2.1.3 https://actuaries.org.sg/sites/default/files/2021-01/SASResponseMSH LReview2020FI NAL.pdf

16 CAGR - Compound Annual Growth Rate

27 Instead of repeatedly lamenting that healthcare providers and policyholders are to blame for the losses incurred by some IP insurers through overconsumption, overservicing and overcharging, IP insurers should take the necessary steps to explore cutting their own management and commission costs to enhance the sustainability of the IP sector. The relevant authorities should take a look at overseas practices. In USA, the Affordable Care Act or "Obamacare" formally states that insurers must spend at least 80-85% of premiums on health costs17; rebates to policyholders must be issued if this is violated. As one can see from Table 1 (paragraph 24), only 75% of premiums collected are paid as claims in 2019 for the IP sector.

28 Since the IP sector is already subsidised indirectly by the government through voluntary downgrading, the SMA recommends that the relevant authorities impose a 85% or 90% claims ratio on each IP insurer, to instil cost discipline in IP insurers and ensure that premiums collected are directed to healthcare costs and not frittered away on non -healthcare cost items.

The Case for Improving Efficiency in the IP Sector

29 Perhaps a larger question that needs to be asked is whether we need seven IP insurers to operate the entire IP sector. Each IP insurer carries with itself certain costs: cost of setting up management infrastructure that includes senior management, claims management, marketing, insurance agent network, as well as compliance costs and others, just to mention few. Therefore it is safe to say that the current IP sector is carrying the costs of seven sets of senior management, claims management departments and so on.

30 Many studies have shown that a single-payor system, while limiting consumer choice, is the most cost-effective. One should wonder, did MOH soak up $166M in management costs to run Medishield Life in 2019? Although figures are not available, we think not. More money was spent on commissions than management costs in 2019. This could be because there are many insurance agents and financial advisors representing so many IP insurers that have to be paid, even though the market penetration rate is unlikely to grow beyond the current 70% by very much going forward.

31 In the long term, the SMA Council believes that the IP sector could be well served by being managed and operated by fewer payors. Ideally, a single payor would be preferred. This will weed out the current inefficiencies that bedevil the current environment, in particular:

a) Duplication of resources and costs by having too many IP insurers

b) Management and commission costs growing at a much faster rate than growth in claims, that is, actual healthcare being delivered

17 https://www.healthcare.gov/health-care-law-protections/rate-review/

32 Take the figure of $363M that was spent on Management Expenses and Commission in 2019. This is a very sizeable recurrent sum. A single payor can probably run the entire IP sector efficiently and equitably for much less than $363M. Further savings can be achieved from economies of scale under Other Expenses as well. These savings can mitigate future increases in insurance premiums and reduce patients' financial burdens. The case for reduction in number of payors is disruptive, but it is logical. We look forward to hearing from the insurers if they have other solutions to reduce their administrative costs.

Future SMA Initiatives

33 The SMA Council would like to announce two initiatives going forward:

a) Ranking of IP insurers, and

b) Setting up of a SMA Complaints Committee for IPs and Health Insurance.

34 The SMA Council will conduct annual SMA member surveys to rank IP providers. The results will be made public. Some of the parameters used in this ranking exercise will include:

a) Inclusiveness of panels

b) Transparency of doctor selection criteria for panels

c) Ease and timeliness of pre -authorisation process

d) Timeliness of payment

e) Appropriateness of fee scales with respect to MOH fee benchmarks

f) Degree of friction and penalties imposed on policyholders when non -panel doctors are used

35 The SMA Council will also set up a SMA Complaints Committee for IPs and Health Insurance. Doctors and members of the public will be able to freely submit information (with patient identifiers removed if necessary) to this Committee on cases whereby they feel IP providers have:

a) Not provided insurance coverage, organised, delayed or redirected care that are not in the patient's best interests

b) Not adequately reimbursed doctors for services rendered or not paid them in a timely manner

c) Not been fair and equitable to other stakeholders in any way

36 This Committee will refer egregious cases to the relevant authorities for their attention and necessary action. We will also construct a database arising from these complaints to see which IP insurer attracts an inordinate number of complaints.

61st Council

Singapore Medical Association

25 Mar 2021